|

| A 1795 Spanish dollar, minted in Mexico, with several chopmarks |

One of the most interesting things about bitcoin, ripple, and other cryptocurrencies is how they are maintained by a dispersed user base rather than some central issuing authority. These users (miners in the case of bitcoin, nodes for ripple) ensure that each "coin" is a legitimate member of the total population of cryptocoins comprising that particular ledger. They are what stand between good coin and bad coin.

I've run into two historical cases of a dispersed method of policing of the quality of exchange media: the endorsement of bills of exchange and the chopmarking of silver coins. It may be worthwhile to explore these two cases.

The Watchdog role

The watchdog or verification function is an important one, especially in anonymous trade where the unlikelihood of a repeat meeting between buyer and seller increases the incentives to be dishonest and pass off lousy coin. Not-so-liquid goods, say sofas, are insulated from the bad coin problem. Due to physical characteristics that impede their liquidity, sofas tend to be sold from fixed locations, or shops. Because a merchant is shackled to his shop and thus unable to preserve his anonymity, any attempt to pass off bad sofas will hurt his business reputation. In the end, only good sofas get stocked by the merchant.

Unfortunately for him, the merchant faces the danger that his much more mobile customers may try and sell him bad coin. The merchant can always threaten them with an embargo should they fob off a fake, but his customers will simply avoid his penalty by shopping at a competing merchant the next time they want a sofa.

In the case of paper money and coinage, the merchant is somewhat protected from the bad coin problem by difficult-to-counterfeit designs printed on the bill or engraved on a coin's face by the issuing authority. In the case of bank money, he is protected by the owners of the credit card networks who approve the legitimacy of a card prior to consummation of trade. These are centralized watchdog systems. What is interesting is that a number of decentralized, or dispersed systems have evolved in times past to offer further protection, including the use of chopmarks:

Chopmarking

In the 16th C, Spanish silver dollars, or pieces of eight, began to appear in China. These coins were minted in Spanish-controlled Mexico, shipped by Spanish vessels to the Philippines where they were exchanged for Chinese goods like porcelain and spices, and finally brought to China by Chinese and other foreign merchants.

Minted on the reverse side with a Christian cross and the obverse side with a Spanish coat of arms, and covered over with Latin characters, the patterning of the Spanish dollar would have meant little to the typical Chinese consumer or merchant. In fact, any pattern would have done just as well since silver was traditionally not accepted at its face value in China, but by its weight (this contrasts to the west, where Spanish dollars were typically accepted at face value). This may have been partly due to the fact that silver ingots, or sycee, had circulated in China long before the piece of eight ever made an appearance, with each city having its own particular standard. Because these sycee circulated according to weight, prior to consummating a trade, merchants would use a set of scales, or dotchin, to determine the value of each ingot.

While anyone with a set of scales could easily ascertain the weight of a particular coin, the difficult part would have been determining the purity of that coin. Counterfeit Spanish dollars were not uncommon, after all, but not everyone would have had the skills to detect them. This is where chopmarking came in handy. Merchants and professional money exchangers, or shroffs, would assay a coin to verify its silver content. The theory goes that once the coin had passed their purity test, a shroff would stamp that coin with his own peculiar chopmark—a Chinese character, an emblem, symbol, or a pseudo character.

Numismaticist Bruce Smith describes the reason for chopping thusly:

I think the chop was only a guarantee that it was acceptable silver. It didn't really matter if the coin was genuine or not. As long as it had the right weight and right fineness as far as they could tell. I mean they were only looking at it by eye and by sound. If it looked like the silver was good and it sounded good [the ‘ring’] and the weight was acceptable then it was okay.According to Frank Rose, a numismatist who published an early text on chop marks, certain merchants chopmarked every legitimate coin that came into their possession and would readily take back any coin bearing one of their earlier marks. So by chopmarking a coin, a merchant would have been taking on a liability of his own, almost as if he had issued a redeemable paper note or a deposit.

In any case, foreign coins often became so covered in chop marks during the course of trade that their initial design became unrecognizable, as the coin below shows.

MFIckJe2q-BSbuvlSI,g~~60_1.JPG)

The genius of this system is that a naive Chinese consumer could safely accept a coin knowing that as long as it was chopped it had successfully passed the smell test of professional appraisers--and the more chops the better. Chopping, like bitcoin mining, transformed a virgin coin into the native exchange medium, with chopmarks serving as a way for disparate users to verify a coin's membership in the set of good silver pieces.

Endorsing

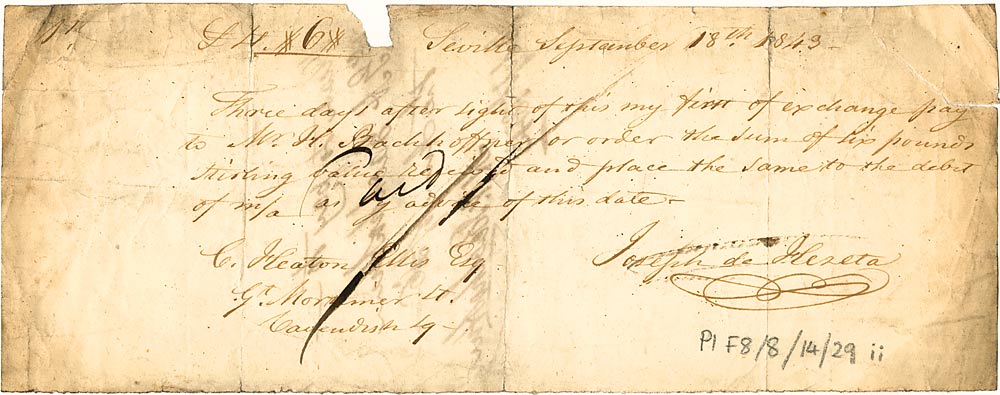

Another interesting form of dispersed verification was the system of bills of exchange, especially the system that developed in Lancashire, a county in northern England. A bill of exchange was a paper contract between two sides in a transaction. It was created or 'drawn' up by the person who provided goods or services, the 'drawer'. The counterparty who had taken position of goods stood as the 'acceptor' and by signing the bill, promised to render up a certain amount of coins to the drawer, usually three months hence. The drawer kept the bill in his desk until three months had passed upon which he presented it to the acceptor, got his gold, and the two parted ways.

|

| A bill of exchange, 1843 [link] |

When the bill was due the third party could call on the original acceptor for payment, even though the original agreement had been between the drawer and the acceptor. Should the third party find the acceptor unable to pay the gold upon maturity, he could make a claim on the endorser for full payment. Alternatively, the third party could in turn endorse the bill on to someone else, who could it turn endorse it to someone else, etc. turning what had been an illiquid bill into a highly liquid and potent medium of exchange.

This is exactly what happened in Lancashire, according to this paper by T.S. Ashton. Not only were bills used by large scale industry, but according to Ashton they were used in small transactions too. While coin was generally reserved for the payment of wages, those a little higher in economic status than hired workers, small-capitalist spinners and small time manufacturers with an apprentice or two, were induced to accept payment in Lancashire bills. According to Henry Thornton, who Ashton quotes, all payments at Liverpool and Manchester - then part of Lancashire - were carried out either in coin or bills of exchange. Henry Dunning Macleod describes bills "which had sometimes 150 indorsements on them before they became due."

The practice of endorsement was hugely advantageous for the general populace, for as Ashton points out:

"Since each successive holder endorsed it, the more it circulated the greater the number of guarantors of its ultimate payment in cash. Even if some of the parties to it should be men of doubtful credit it might still circulate, for it was unlikely that they would go down simultaneously."So in the same way that multiple chop marks and blockchain confirmations ensure that a coin is a good one, multiple endorsements converted an IOU into a member of the population of verified IOUs, and therefore suitable for broad circulation. In the end, what bitcoin and the other cryptocoins is certainly novel, but we have seen parts of this story before.

Comments

Post a Comment